Fascination About Tulsa Bankruptcy Lawyer

Some Known Facts About Tulsa Debt Relief Attorney.

Table of ContentsSee This Report on Tulsa Debt Relief Attorney9 Easy Facts About Affordable Bankruptcy Lawyer Tulsa ExplainedBest Bankruptcy Attorney Tulsa Fundamentals ExplainedThe Best Guide To Tulsa Bankruptcy Consultation10 Easy Facts About Chapter 7 - Bankruptcy Basics Shown

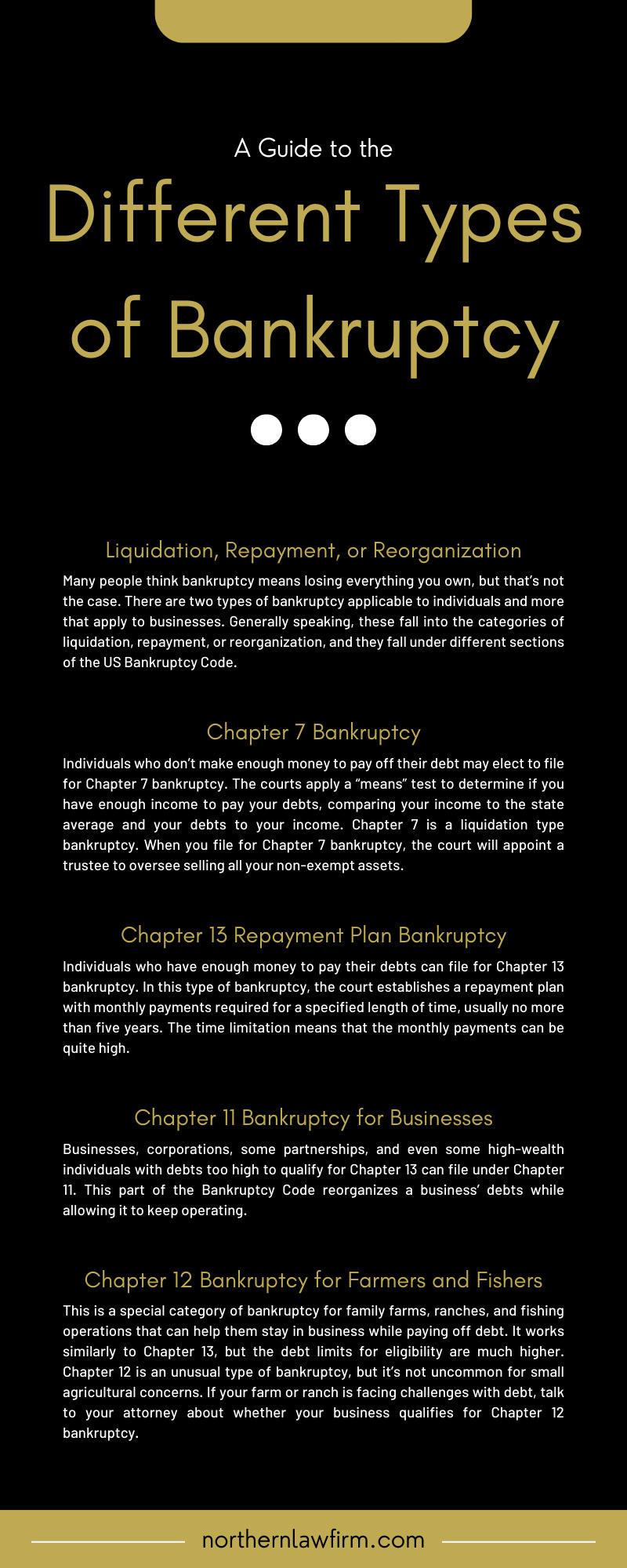

The statistics for the other primary kind, Phase 13, are also worse for pro se filers. Suffice it to state, talk with a legal representative or 2 near you who's experienced with insolvency regulation.Lots of attorneys additionally use complimentary consultations or email Q&A s. Take advantage of that. Ask them if bankruptcy is undoubtedly the appropriate selection for your situation and whether they assume you'll certify.

Advertisements by Money. We may be compensated if you click this advertisement. Advertisement Now that you have actually chosen bankruptcy is indeed the best strategy and you with any luck removed it with an attorney you'll need to start on the documentation. Before you study all the main bankruptcy forms, you should obtain your own documents in order.

Getting The Experienced Bankruptcy Lawyer Tulsa To Work

Later on down the line, you'll actually need to show that by divulging all kind of details concerning your economic events. Below's a standard checklist of what you'll need on the roadway in advance: Recognizing records like your chauffeur's permit and Social Safety and security card Income tax return (up to the past 4 years) Proof of income (pay stubs, W-2s, independent earnings, income from assets in addition to any kind of earnings from federal government advantages) Bank statements and/or retired life account statements Evidence of worth of your properties, such as car and actual estate assessment.

You'll wish to understand what sort of debt you're attempting to resolve. Debts like youngster assistance, spousal support and certain tax financial obligations can not be released (and bankruptcy can't stop wage garnishment relevant to those financial debts). Student funding financial debt, on the other hand, is possible to release, however note that it is challenging to do so (Tulsa OK bankruptcy attorney).

You'll wish to understand what sort of debt you're attempting to resolve. Debts like youngster assistance, spousal support and certain tax financial obligations can not be released (and bankruptcy can't stop wage garnishment relevant to those financial debts). Student funding financial debt, on the other hand, is possible to release, however note that it is challenging to do so (Tulsa OK bankruptcy attorney).If your earnings is too expensive, you have an additional alternative: Phase 13. pop over to this website This option takes longer to fix your debts since it calls for a long-lasting settlement strategy usually three to five years before several of your remaining financial obligations are wiped away. The declaring procedure is also a great deal a lot more complicated than Chapter 7.

Some Of Chapter 7 Bankruptcy Attorney Tulsa

A Chapter 7 insolvency stays on your credit score record for ten years, whereas a Phase 13 insolvency falls off after 7. Both have enduring influence on your credit rating, and any brand-new financial debt you get will likely feature greater rate of interest. Prior to you send your insolvency types, you should first finish an obligatory training course from a credit rating therapy agency that has been accepted by the Department of Justice (with the significant exception of filers in Alabama or North Carolina).

The course can be completed online, in person or over the phone. You should complete the program within 180 days of filing for personal bankruptcy.

The smart Trick of Tulsa Bankruptcy Consultation That Nobody is Discussing

Examine that you're submitting with the appropriate one based on where you live. If your irreversible residence has actually relocated within 180 days of filling, you need to submit in the area where you lived the better section of that 180-day duration.

Typically, your personal bankruptcy attorney will function with the trustee, yet you may require to send out the person files such as pay stubs, tax returns, and financial institution account and credit report card statements straight. A common mistaken belief with bankruptcy is that when you file, you can quit paying your financial obligations. While bankruptcy can aid you wipe out numerous of your unsecured financial debts, such as overdue medical bills or personal loans, you'll desire to maintain paying your monthly my link payments for guaranteed financial debts if you desire to keep the home.

Not known Details About Tulsa Bankruptcy Legal Services

If you go to risk of repossession and have actually exhausted all various other financial-relief choices, after that declaring Phase 13 might postpone the repossession and assistance conserve your home. Eventually, you will still require the earnings to continue making future home mortgage settlements, along with paying back any kind of late payments over the program of your settlement plan.

The audit can postpone any financial obligation alleviation by numerous weeks. That you made it this much in the procedure is a good sign at the very least some of your financial obligations are eligible for discharge.